U.S. Data Center Lead and What It Means

Consider: “The U.S. has 3,960 data centers in this dataset – more than the next 14 countries combined.” At this rate, the US on the verge of total capture by AI. This includes governance, industry, medical, surveillance, finance and endless AI Psychosis. As AI continues to double in capability about 4 1/2 months and GPU breakthroughs doubling every 6 months, America is cooked. ⁃ Patrick Wood, Editor.

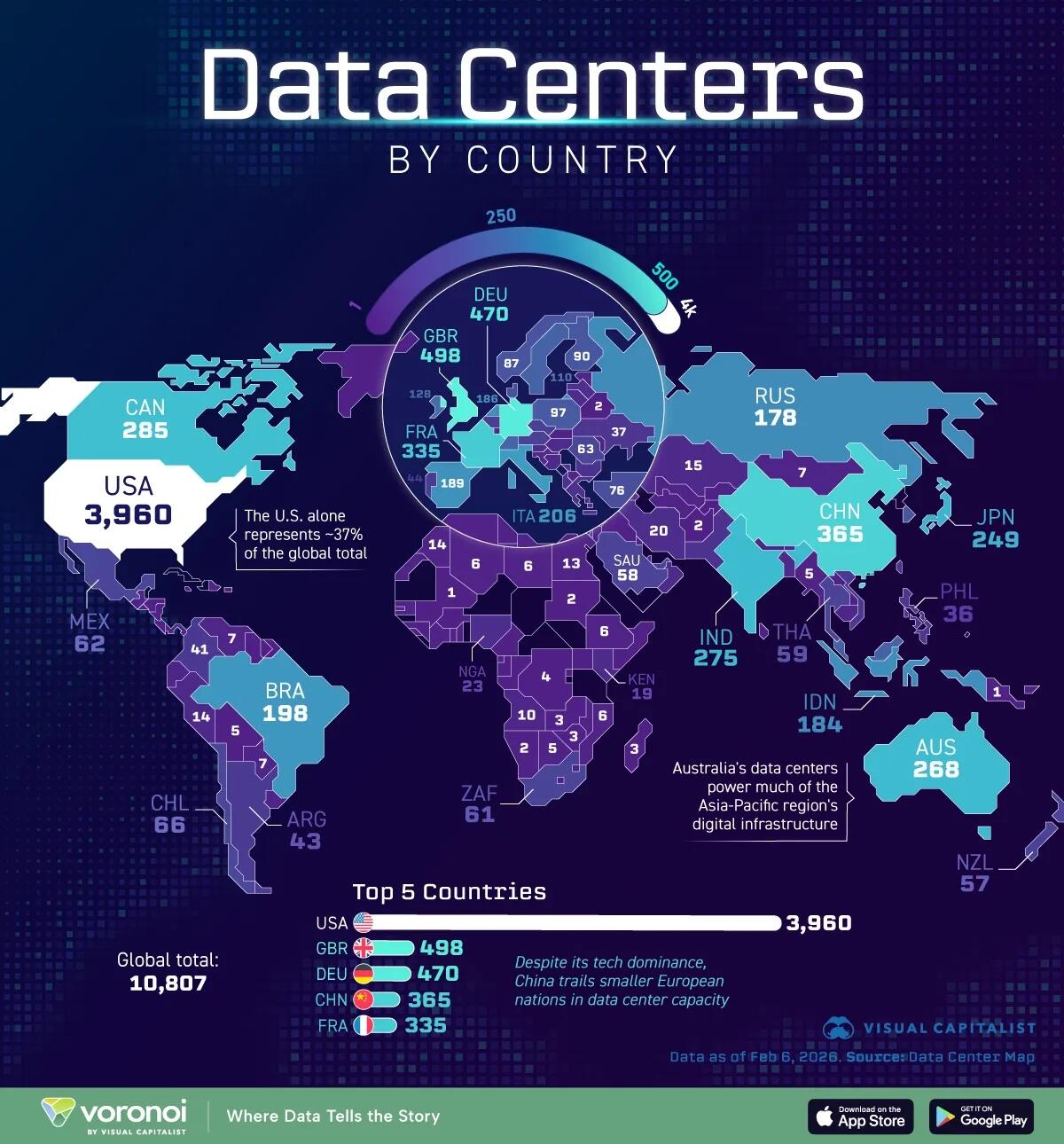

Data centers are the physical backbone of streaming, cloud storage, and modern AI systems. The concentration of facilities shapes where compute, data, and influence sit. That geography matters for industry, regulation, and resilience.

The U.S. has 3,960 data centers in this dataset – more than the next 14 countries combined.

The figure above comes from a country-by-country facility count compiled from public data and industry directories. Different methodologies shift totals, but the broad pattern is clear: a handful of economies host most capacity. Hyperscale cloud investments concentrate infrastructure where customers, power, and fiber converge.

Top national counts from the dataset include:

- USA — 3,960

- United Kingdom — 498

- Germany — 470

- China — 365

- France — 335

- Canada — 285

- India — 275

- Australia — 268

- Japan — 249

- Italy — 206

- Brazil — 198

- Spain — 189

- The Netherlands — 186

- Indonesia — 184

- Russia — 178

Those counts include everything from modest cloud hubs to sprawling colocation campuses that handle hyperscaler workloads. They reflect where firms have chosen to site capacity for latency, tax, and regulatory reasons. The U.S. lead is especially driven by major cloud providers and long-term private investment.

Some industry observers count more facilities by widening the definition of a data center, and those estimates can push the U.S. total above 5,000. Regardless of the exact number, the imbalance in capacity is large enough to shape global technology relationships. That reality touches supply chains, national security planning, and corporate strategy.

Europe holds the second-largest concentration overall, with the UK, Germany, and France each hosting hundreds of facilities. Regional peering points and dense markets make Western Europe an attractive location for multinational IT services. Smaller European nations often specialize in connectivity, dark fiber, or financial services hosting.

Asia is growing fast, led by China, Japan, and India, with expansion driven by mobile adoption and cloud migration. Southeast Asian markets such as Indonesia and Malaysia are emerging as demand rises, while Singapore and Hong Kong serve as critical connectivity hubs. National strategies and local regulation will shape how capacity spreads across the region.

A full global list shows many mid-size and small markets with single- to double-digit facilities, illustrating that digital infrastructure is nearly everywhere. That spread matters for redundancy and local services, even if global compute remains concentrated. For planners and policymakers, the distribution of data centers is a practical indicator of where economic and digital power is stacked.